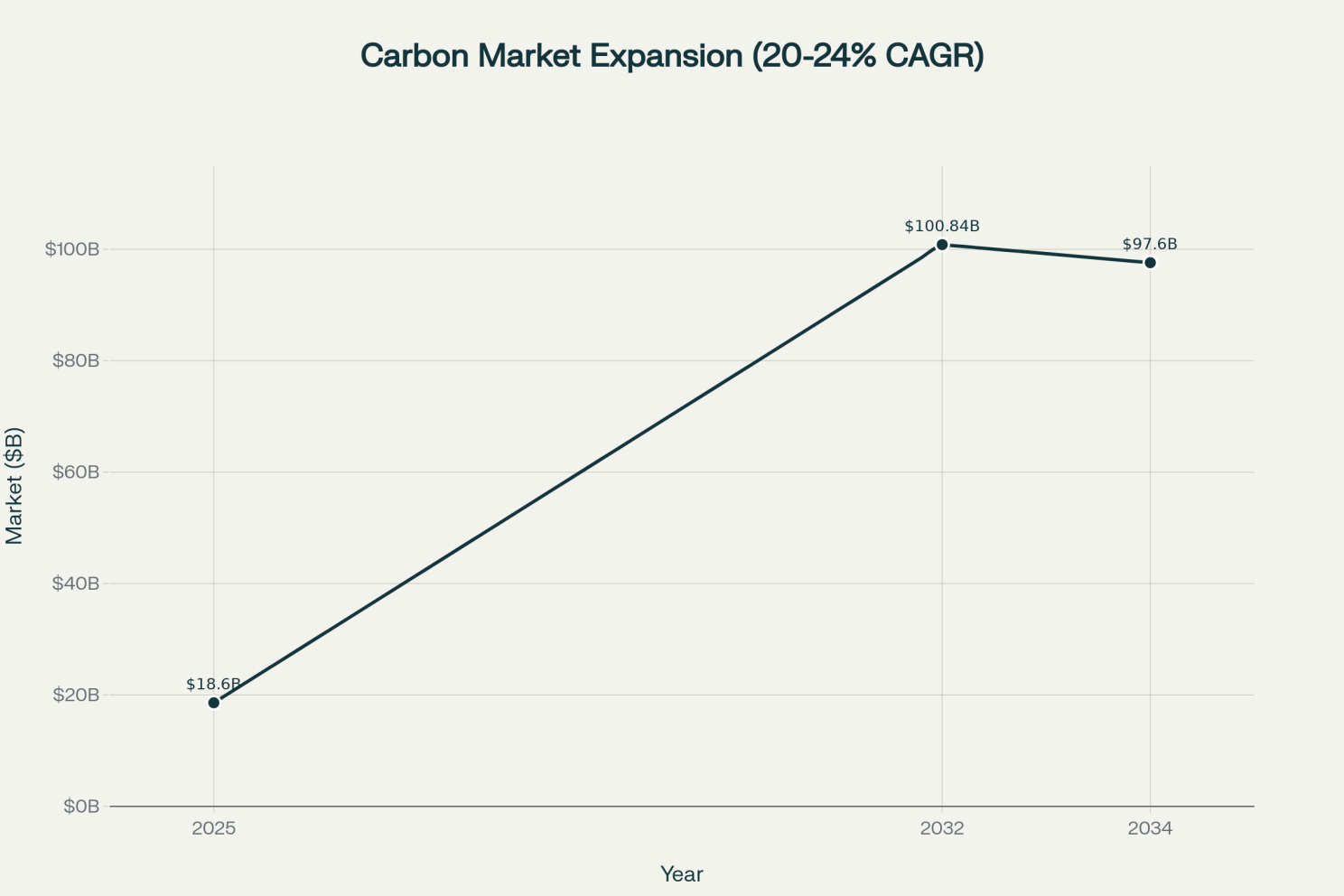

The convergence of regulatory pressure, investor expectations, and technological innovation has elevated sustainability transformation and carbon accounting from a compliance exercise to a strategic imperative. With 98% of Fortune 100 companies committing to sustainability and the carbon accounting software market projected to surge from $18.6 billion in 2025 to over $100 billion by 2032, corporate leaders face both unprecedented challenges and remarkable opportunities. This transformation encompasses three critical pillars: net-zero commitment implementation driving revenue under such commitments from $3.8 trillion to $26.4 trillion among 929 companies, real-time emissions monitoring through advanced technology platforms, and comprehensive supply chain decarbonization integrated with ESG frameworks. The stakes are substantial—organizations that successfully navigate this transition unlock competitive advantages including enhanced access to capital, operational cost reductions averaging 8-10%, and positioning within the $42.6 billion sustainability market growing at 16.8% CAGR.

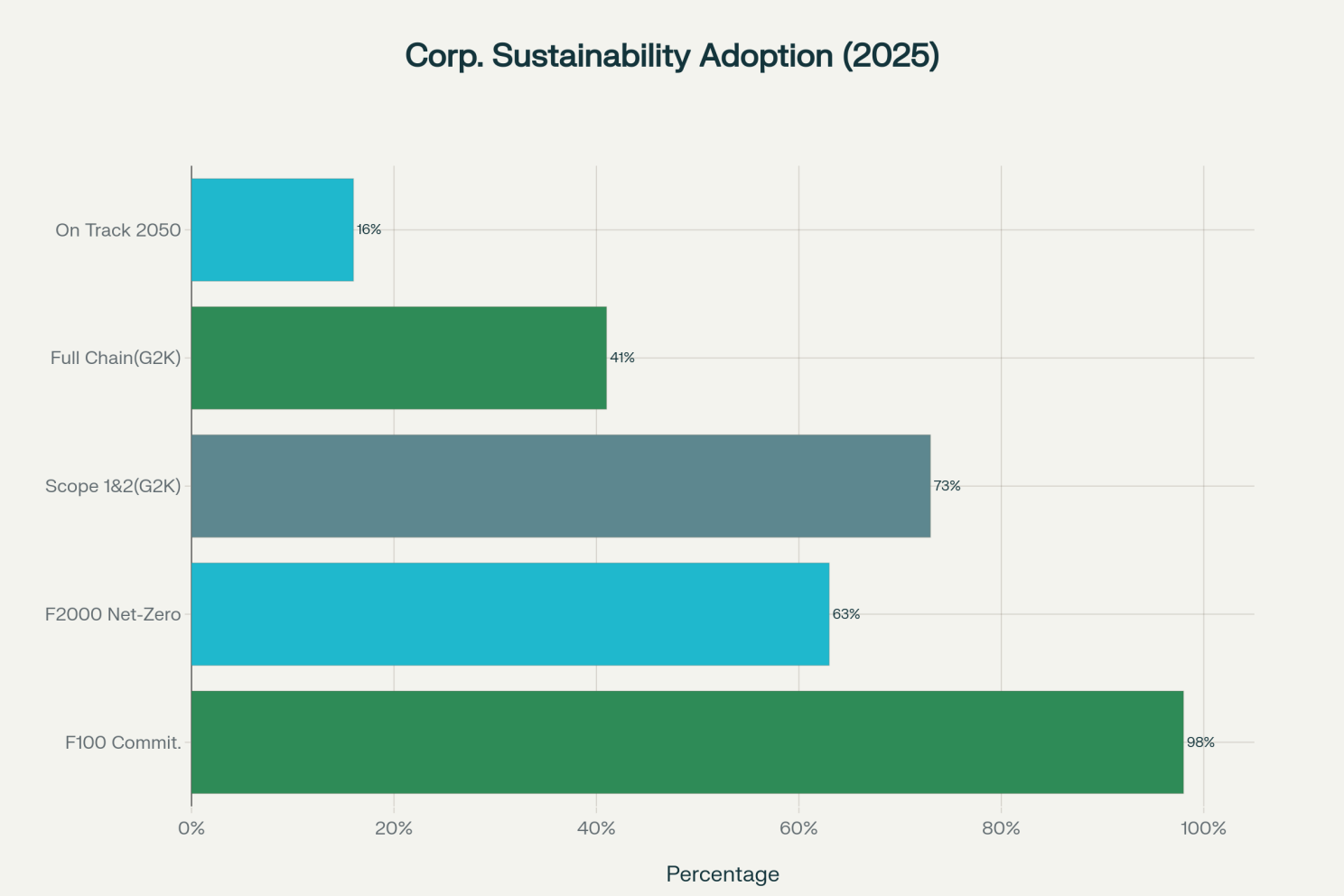

Corporate sustainability adoption varies significantly across commitment levels, with 98% of Fortune 100 companies having sustainability commitments but only 16% on track to achieve 2050 net-zero targets

The sustainability transformation market represents one of the most significant business opportunities of the 21st century. Valued at $42.6 billion by 2025, this market continues expanding at a 16.8% compound annual growth rate, driven by regulatory mandates, investor pressure, and competitive differentiation. Within this broader landscape, carbon accounting software has emerged as a critical enabler, with market valuations ranging from $18.6 billion to $22.51 billion in 2025, projected to reach between $97.6 billion and $100.84 billion by 2032-2034. This explosive growth—representing a CAGR of 20.2% to 23.9%—reflects the fundamental shift in how corporations measure, manage, and monetize their environmental impact.

The financial implications extend far beyond software investments. Companies with high ESG scores receive cost of capital discounts averaging 10% compared to lower-scoring peers, while ESG leaders in 2021 achieved returns 8% higher than broader market indices. More dramatically, organizations demonstrating strong sustainability performance significantly outperform counterparts over the long term, with sustainable initiatives increasing shareholder value by an average of $1.28 billion over 15-year periods.

These returns stem from multiple value drivers: energy efficiency improvements yielding immediate cost savings, enhanced brand reputation attracting premium pricing, risk mitigation reducing insurance and financing costs, and preferential access to $1 trillion+ in sustainable finance commitments from institutions like Bank of America.

The carbon accounting software market is projected to grow from $18.6 billion in 2025 to over $100 billion by 2032, representing a CAGR exceeding 20%

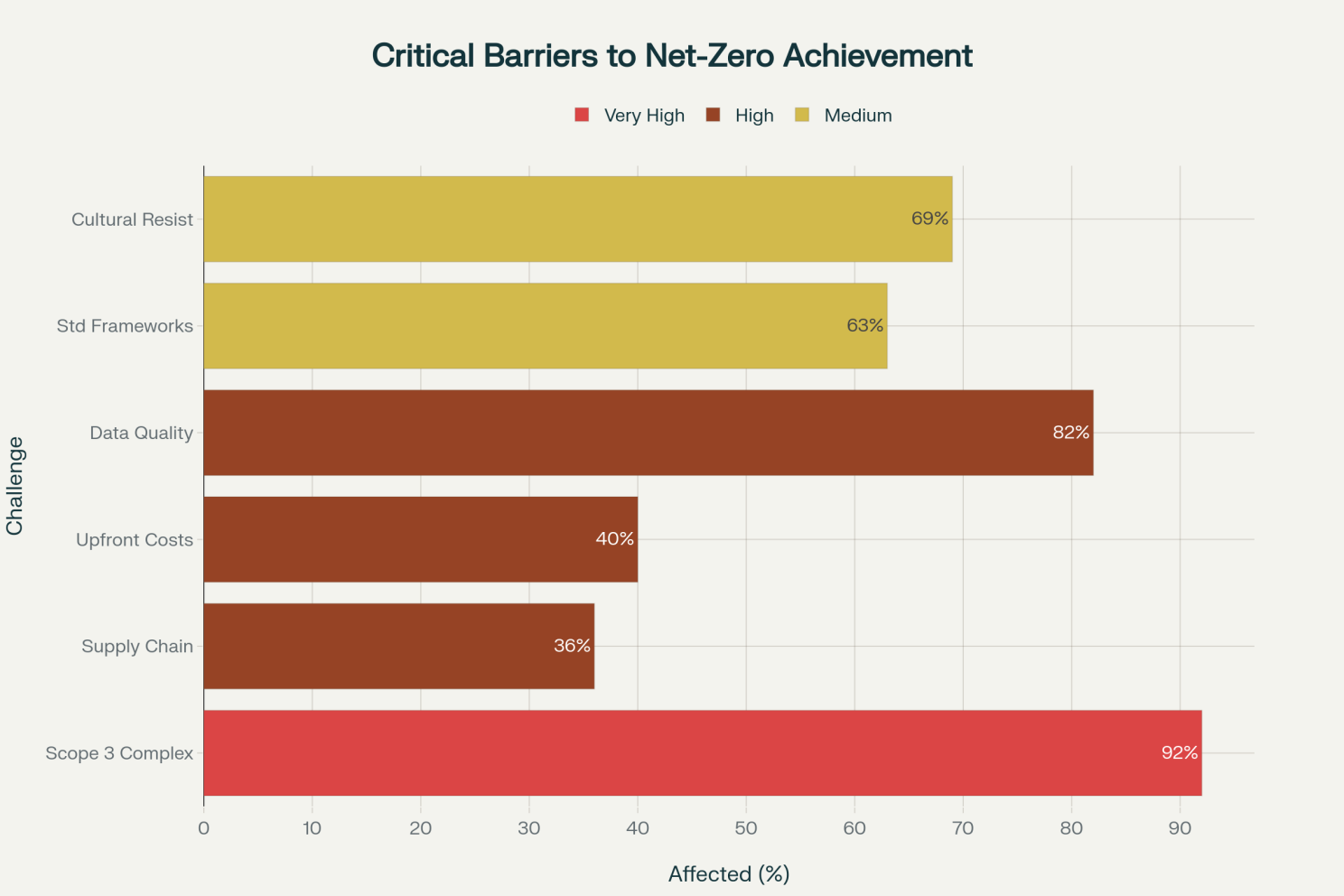

Yet the opportunity comes with substantial execution risk. Despite widespread commitments, only 16% of large companies remain on track to achieve 2050 net-zero targets, representing a mere 4% of total global emissions from assessed entities. This implementation gap—what we might term the “ambition-execution chasm”—creates both competitive vulnerability for laggards and strategic opportunity for organizations that develop robust carbon accounting and decarbonization capabilities.

The regulatory environment has undergone seismic shifts, creating a complex patchwork of mandatory disclosure requirements. While the U.S. Securities and Exchange Commission withdrew its defense of federal climate disclosure rules in March 2025, California, Illinois, and Colorado have enacted state-level requirements, and the European Union’s Corporate Sustainability Reporting Directive (CSRD) mandates comprehensive climate and sustainability reporting for companies with EU operations beginning in 2025. The CSRD applies to approximately 50,000 companies, including U.S. firms with significant European presence, requiring detailed disclosures on Scope 1, 2, and in many cases, Scope 3 emissions.

Internationally, 36 jurisdictions had adopted or were implementing the International Sustainability Standards Board (ISSB) framework as of June 2025, creating a de facto global standard for climate-related financial disclosures. These frameworks require companies to disclose governance structures overseeing climate risks, strategic responses to physical and transition risks, risk management processes, and quantitative metrics including greenhouse gas emissions across all material scopes. The multiplicity of frameworks—with over 600 ESG standards globally according to Ernst & Young—creates both complexity and opportunity for organizations that develop integrated reporting capabilities.

Corporate penalties for non-compliance or greenwashing have escalated dramatically. Regulatory bodies increasingly scrutinize sustainability claims, with fines reaching material percentages of revenue for companies providing inaccurate emissions data or misleading climate commitments. Beyond regulatory sanctions, reputational damage from failed sustainability commitments can permanently impair brand value and stakeholder relationships, particularly given that 89% of institutional investors now incorporate ESG data into investment decisions.

Want an implementation framework? Subscribe to our newsletter [Gear Up]. Where S&H Designs, a team of “Innovative Minds”, “Empowering decision makers with actionable insight.”

Corporate net-zero commitments have reached extraordinary scale, with 63% of Forbes Global 2000 companies—representing 1,245 organizations with combined revenue of $36.6 trillion—now having established net-zero targets. This represents a remarkable acceleration from just 769 entities in December 2020 to 1,935 entities with net-zero or similar targets by September 2025. Among the most sophisticated cohort, 41% of the largest 2,000 global companies have set value chain net-zero targets covering Scopes 1, 2, and 3 emissions, up from 37% in 2023-2024 and 27% in 2021. Notably, corporate commitment growth persisted even amid political headwinds, with U.S. company net-zero targets increasing 9% in 2024-2025 to encompass 304 organizations representing $12 trillion in revenue.

The revenue under net-zero corporate commitments has surged from $3.8 trillion to $26.4 trillion among the 929 companies setting such targets, demonstrating that sustainability transformation has moved from the periphery to the core of global commerce. This financial scale positions corporate decarbonization as a primary lever for achieving Paris Agreement goals, given that the 164 Climate Action 100+ focus companies collectively account for over two-thirds of global industrial greenhouse gas emissions with a combined market capitalization exceeding $8 trillion.

The Science Based Targets initiative (SBTi) has emerged as the gold standard for corporate climate target validation, with its Corporate Net-Zero Standard providing the only framework for corporate net-zero target setting aligned with climate science. The standard requires companies to commit to near-term targets delivering rapid, deep cuts to roughly halve emissions before 2030, long-term targets cutting more than 90% of emissions before 2050, and neutralization of residual emissions through permanent carbon removal and storage. As of 2025, SBTi has validated targets for thousands of companies across sectors, with commitments increasingly including comprehensive Scope 3 coverage.

However, target quality varies considerably. While 85% of companies assessed by Climate Action 100+ have set medium-term greenhouse gas reduction targets and 80% have established long-term targets, only 9% of focus companies have emissions targets aligned with (or exceeding) the minimum Paris Agreement goal of limiting temperature rise to below 2°C. This “ambition gap” reflects the difficulty of translating headline commitments into science-based decarbonization pathways, particularly for carbon-intensive sectors like energy, materials, and transportation.

The planning gap presents an equally significant challenge. Across Forbes Global 2000 companies with net-zero targets, nearly one in three (385 companies representing 31% of commitments) lack detailed transition plans backing their pledges. Without accompanying plans specifying decarbonization levers, technology deployments, capital allocation, and implementation timelines, targets risk becoming aspirational statements rather than actionable roadmaps. Forward-thinking organizations address this by developing comprehensive transition plans that identify and sequence rollout of decarbonization levers, integrate climate considerations into core business strategy, and function as living documents capturing rapidly changing technological and regulatory landscapes.

Translating net-zero commitments into operational reality requires substantial capital deployment. Survey data indicates 83% of global executives increased sustainability investments in the past year, with nearly one in seven reporting increases exceeding 20%. The largest companies are allocating 58% of their capital investments to sustainable projects in 2023, up from 55% in the prior year and dramatically exceeding the 15% sustainable investment rate among smaller publicly traded companies. This investment prioritization reflects recognition that sustainable capital expenditure is growing twice as fast as all other capex, with sustainable revenues expanding at double the rate of other revenues.

Specific investment categories attracting capital include renewable energy procurement and development, energy efficiency technologies such as LED lighting and HVAC optimization, building-related decarbonization measures, waste reduction and circular economy initiatives, and supplier engagement programs. The most advanced organizations implement internal carbon pricing mechanisms—with prices ranging from $10 to $100+ per ton of CO2 equivalent—to guide capital allocation decisions and incentivize business units to pursue emission reductions. Microsoft’s carbon-negative commitment by 2030 exemplifies this approach, backed by a billion-dollar Climate Innovation Fund and internal carbon taxes applied to business units to fund decarbonization initiatives.

Despite growing investment levels, capital constraints remain a primary barrier, particularly for small and medium-sized enterprises. Forty percent of SMEs cite insufficient budgets and high costs as major obstacles to achieving net-zero.

Innovative financing mechanisms are emerging to address this challenge, including green bonds offering lower interest rates due to reduced risk profiles, sustainability-linked loans with interest rates tied to ESG performance metrics, government subsidies and tax incentives for clean energy and efficiency investments, and energy-as-a-service contracting models that eliminate upfront capital requirements.

Organizations that creatively leverage these financing tools gain competitive advantages in accelerating their sustainability transformations.

To know more, contact us at design@shdesigns.in

The sustainability ecosystem is undergoing a fundamental shift from static, quarterly environmental reports to dynamic, real-time compliance and decision-support systems. Continuous Emissions Monitoring Systems (CEMS) are now mandatory in many industrial sectors, enabling regulators, investors, and company leadership to access instant transparency and automated accountability. This transformation reflects both technological capability—with sensors, IoT networks, and AI analytics reaching maturity—and stakeholder expectations for up-to-the-minute emissions data.

Advanced monitoring platforms reduce data reporting latency from 24 hours to just one hour while increasing spatial resolution from 30 meters to 10 meters and enhancing detection accuracy from 80% to 95%. These improvements stem from integration of multiple data sources and analytical techniques: satellite-based remote sensing providing geographic coverage, ground-based IoT sensor networks delivering granular facility-level data, artificial intelligence and machine learning algorithms identifying patterns and anomalies, and blockchain-enabled data integrity ensuring tamper-resistant audit trails.

Real-time emissions intelligence transforms carbon from an abstract reporting metric into an operational variable that influences daily business decisions. Organizations can now monitor emissions alongside traditional performance indicators like throughput, quality, and cost, enabling managers to optimize for carbon efficiency in real-time rather than discovering emissions profiles months after the fact during periodic reporting cycles. This operational integration represents a maturation of carbon management from compliance function to core business process.

Artificial intelligence has emerged as a transformative force in carbon accounting and emissions reduction. Eighty-one percent of global executives report already using AI to advance sustainability efforts, with another 16% planning deployment within the next year. AI applications span the carbon management value chain: tracking emissions and optimizing energy use, developing new low-carbon products and services, modeling climate-related risks and scenario planning, improving operational efficiency to cut emissions, and automating complex calculations for Scope 3 emissions.

Machine learning models achieve substantial performance improvements over traditional methods. Research demonstrates AI systems reducing data reporting latency by 96% (from 24 hours to 1 hour), increasing detection accuracy by 19% (from 80% to 95%), enhancing spatial resolution by 67% (from 30m to 10m), and identifying previously unknown emission sources while forecasting future trends with high correlation coefficients exceeding 0.9. These capabilities prove particularly valuable for Scope 3 emissions—which represent 92% of an organization’s total greenhouse gas footprint on average yet remain notoriously difficult to measure accurately.

Convolutional neural networks (CNNs) and long short-term memory (LSTM) networks enable sophisticated analysis of satellite imagery and time-series data to detect emission events, quantify concentrations of specific greenhouse gases beyond CO2 (including methane, nitrous oxide, and fluorinated gases), and predict emission trajectories under different operational scenarios. Computer vision systems combined with spectral analysis can automatically identify industrial facilities, classify their operational status, and estimate emissions without relying on self-reported data from facility operators—a capability with profound implications for third-party verification and regulatory enforcement.

IoT sensor deployments create the data foundation for real-time carbon intelligence. Smart devices continuously monitor energy consumption (electricity, natural gas, fuel oil), water usage, production volumes and operational parameters, waste generation and composition, and transportation and logistics activities. These sensors connect to centralized data platforms that aggregate, validate, and analyze information streams, generating actionable insights for facility managers, sustainability teams, and executive leadership.

Practical implementations demonstrate significant impact. GaiaHub’s license plate recognition technology deployed in Liepāja, Latvia, uses computer vision to identify vehicle types at Low Emissions Zone entry points, matches license plates with national vehicle registries containing fuel type and specifications, and calculates real-time emissions considering speed, acceleration, and vehicle-specific factors.

This system enables city officials to monitor traffic emissions continuously rather than waiting for time-consuming data requests to fuel stations and expert analysis, fundamentally improving the speed and accuracy of urban carbon management.

General Electric’s digital wind farm initiative illustrates industrial applications. By deploying sensors across wind turbine components and creating digital twin simulations, GE optimized each wind farm to generate up to 10% more renewable energy, directly increasing the global renewable energy mix while improving operational efficiency and reducing maintenance costs. Similar IoT applications enable energy companies to assess electricity consumption in real-time, matching supply closely with demand and minimizing greenhouse gas emissions from energy storage inefficiencies.

Satellite-based emissions monitoring provides unprecedented geographic coverage and third-party verification capabilities. Platforms like Sentinel-5p, Landsat, and Climate TRACE deliver high-resolution data on greenhouse gas concentrations across extensive regions, enabling detection of emission events invisible to ground-based systems. Remote sensing offers several strategic advantages: feasibility and low cost through open-source data access, reliable monitoring frequency independent of facility operator cooperation, widespread coverage of remote or uncooperative facilities, and third-party validation of corporate emissions claims.

Advanced systems integrate spectral band data from geostationary satellites with deep learning frameworks combining convolutional neural networks, bidirectional LSTM models, and attention mechanisms to estimate daily carbon emissions and electricity generation from fossil fuel power plants simultaneously. These models do not require extra physical or environmental data, making continuous monitoring feasible for practical operations and regulatory oversight. Climate TRACE exemplifies this approach, harnessing technology to track greenhouse gas emissions with unprecedented detail and speed, supporting meaningful climate action by governments, investors, and civil society.

The validation potential of satellite monitoring extends beyond atmospheric concentrations to direct observation of emission sources. Computer vision algorithms can identify industrial facilities, oil and gas infrastructure, agricultural operations, and transportation networks, classifying their operational status and estimating emissions based on observable characteristics. This capability enables regulators and investors to independently verify corporate emissions reports, identifying discrepancies between self-reported figures and satellite-derived estimates. As monitoring technology advances, the gap between claimed and actual emissions performance will become increasingly transparent, raising the stakes for accurate reporting and genuine decarbonization.

Scope 3 emissions—indirect emissions occurring throughout an organization’s value chain beyond owned or controlled assets—represent the most significant and challenging component of corporate carbon footprints. For the average organization, supply chain emissions exceed operational emissions by a factor of 11.4, equating to approximately 92% of total greenhouse gas output. This dominance makes Scope 3 decarbonization essential for any credible net-zero strategy, yet fewer than half of companies with net-zero targets include Scope 3 emissions in their commitments, and even fewer have detailed plans for value chain decarbonization.

The Greenhouse Gas Protocol’s Corporate Value Chain (Scope 3) Standard identifies 15 distinct categories of indirect emissions spanning upstream activities (purchased goods and services, capital goods, fuel and energy-related activities, transportation and distribution, waste, business travel, employee commuting, leased assets) and downstream activities (transportation and distribution, processing of sold products, use of sold products, end-of-life treatment, leased assets, franchises, investments). Organizations must assess which categories are relevant to their operations and material to their carbon footprint, then establish measurement and reduction strategies for each material category.

The complexity stems from multiple factors. Supply chains involve thousands of suppliers across multiple tiers, each with distinct emissions profiles influenced by geography, technology, and operational practices. Data availability varies dramatically—while Tier 1 suppliers increasingly provide direct emissions data, Tier 2 and Tier 3 suppliers typically lack measurement infrastructure, forcing companies to rely on industry-average emission factors and spend-based estimation methods that can overstate or understate actual emissions by orders of magnitude. Methodological inconsistencies compound the problem, with different standards and calculation approaches producing incomparable results that undermine both internal decision-making and external benchmarking.

Organizations employ several approaches to Scope 3 measurement, each with distinct tradeoffs between accuracy and practicality. The spend-based method multiplies economic value of purchased goods or services with industry-average emission factors related to their monetary value, offering simplicity and comprehensive coverage but low accuracy due to averaging across diverse suppliers. The activity-based method uses specific activity data (quantities of materials purchased, distances traveled, waste generated) combined with more granular emission factors, delivering improved accuracy at the cost of greater data collection burden.

Life-cycle assessment (LCA) represents the most comprehensive approach, evaluating emissions across the entire lifecycle of products from raw material extraction through manufacturing, distribution, use, and end-of-life disposal.

LCA methodologies enable identification of emission hotspots within product systems, supporting design decisions that fundamentally reduce embodied carbon rather than simply shifting emissions between lifecycle stages. However, LCA requires detailed technical data and sophisticated modeling capabilities that exceed the resources of many organizations, limiting adoption particularly among small and medium enterprises.

The accuracy gap between methodologies can be substantial. Organizations transitioning from spend-based to activity-based or LCA methods often discover their actual emissions differ from initial estimates by 30-50% or more, with variances in either direction depending on whether industry averages overstate or understate their specific supply chain’s performance. This uncertainty complicates target-setting, progress tracking, and regulatory compliance, making investment in robust Scope 3 measurement capabilities a strategic priority despite significant costs.

Effective supply chain decarbonization requires collaborative partnerships rather than transactional relationships with suppliers. Seventy-nine percent of companies now engage suppliers on emissions reduction as part of their decarbonization strategies, recognizing that mandates without support typically fail while collaborative approaches drive mutual value creation. Leading organizations implement multi-faceted engagement programs including emissions data collection and reporting requirements, capacity building through training and technical assistance, financial incentives or penalties tied to emissions performance, collaborative innovation on low-carbon materials and processes, and supplier rating systems integrating carbon performance with traditional procurement criteria like quality, cost, and delivery.

The Climate Action 100+ initiative demonstrates the power of coordinated engagement. This investor-led coalition bringing together over 600 investors managing more than $68 trillion in assets has secured groundbreaking commitments from focus companies including coal phase-outs, science-based target validation, enhanced Scope 3 emission disclosures, and improved climate lobbying alignment. Case studies reveal significant progress: RWE AG completed coal phase-out and achieved 1.5-degree validation of emission reduction targets by SBTi in January 2025, Ørsted became the first energy company worldwide to reach its 2025 decarbonization target with 98% emissions reduction and 99% renewable energy production, and Enel enhanced climate lobbying disclosures following sustained investor engagement.

However, supplier engagement faces persistent challenges. Thirty-six percent of companies identify supply chain transformation as particularly difficult, citing the need to either work with suppliers to create planet-friendly programs or switch suppliers—decisions with significant business continuity and cost implications. Power dynamics complicate engagement, with large buyers possessing leverage over small suppliers but limited influence over strategically important or monopolistic suppliers. Cultural and geographic factors add layers of complexity, as suppliers in different regions face varying regulatory environments, technological capabilities, and stakeholder pressures that influence their receptiveness to decarbonization requests.

Supply chain sustainability initiatives increasingly integrate with comprehensive ESG reporting frameworks, creating holistic approaches to corporate responsibility that extend beyond carbon accounting to encompass human rights, labor practices, diversity and inclusion, business ethics, and community impact. This integration reflects recognition that sustainability challenges interconnect—for instance, climate change adaptation requires just transition principles ensuring workers and communities dependent on fossil fuel industries receive support as economies decarbonize.

Multiple ESG frameworks guide corporate disclosure, each with distinct emphases and stakeholder audiences. The Global Reporting Initiative (GRI) Standards, used by 75% of G250 companies, focus on broad stakeholder impact and double materiality—assessing both how sustainability issues affect the business and how the business affects society and the environment. The Sustainability Accounting Standards Board (SASB) Standards provide sector-specific metrics for 77 industries emphasizing financially material ESG factors relevant to investor decision-making. The Task Force on Climate-related Financial Disclosures (TCFD) framework, adopted by 73% of G250 companies, structures climate risk disclosure around governance, strategy, risk management, and metrics.

The International Sustainability Standards Board (ISSB) has emerged as a unifying force, developing IFRS S1 (general sustainability disclosure) and IFRS S2 (climate-specific disclosure) standards designed as a global baseline that companies can supplement with other frameworks addressing specific stakeholder needs or regulatory requirements. The ISSB standards incorporate and build upon TCFD recommendations while achieving interoperability with GRI and other major frameworks, reducing duplicative reporting burden for companies operating across multiple jurisdictions. Organizations that implement integrated ESG data management systems—leveraging ERP-centric platforms to consolidate sustainability data with financial and operational information—gain efficiency advantages and improve data accuracy, consistency, and auditability.

Sustainability transformation requires clear governance beginning with board-level oversight. Seventy-seven percent of Climate Action 100+ focus companies have defined board-level responsibility for climate change, and organizations with explicit board oversight demonstrate superior performance on emissions reduction, target achievement, and disclosure quality. Best-practice governance structures include: Board sustainability committees with regular reporting on emissions performance, climate risks, and decarbonization progress; executive compensation linkages with 80% of Global 100 companies incorporating sustainability metrics into pay structures (up from 64% in prior year); Chief Sustainability Officer or equivalent C-suite position with authority and resources to drive transformation; cross-functional sustainability councils integrating carbon considerations across operations, finance, procurement, product development, and investor relations; and science-based targets validated by independent third parties providing objective accountability.

Effective governance transcends reporting structures to embed carbon considerations in core business processes. Only 3% of business leaders express confidence that their organizations have mechanisms to integrate carbon in all investment and business decisions, while 69% report their companies lack incentives for organizations and individuals to achieve decarbonization objectives. Closing this integration gap requires: Internal carbon pricing applied across business units to guide capital allocation and operational decisions; sustainability criteria incorporated into strategic planning, M&A due diligence, and product development processes; carbon performance metrics integrated into enterprise resource planning and business intelligence systems; and regular scenario analysis evaluating business model resilience under different climate policy and physical risk scenarios.

Carbon management technology represents a strategic investment rather than a compliance cost. Organizations should prioritize: Carbon accounting platforms providing automated GHG calculation, emissions tracking across Scopes 1-3, regulatory reporting, and audit-ready documentation—the carbon accounting software market’s explosive growth to $100+ billion by 2032 reflects growing recognition that manual tracking cannot scale to meet increasing disclosure requirements; Real-time monitoring systems integrating IoT sensors, satellite data, and AI analytics to transition from periodic reporting to continuous intelligence enabling dynamic optimization; Supply chain emissions management tools facilitating supplier data collection, hotspot identification, and collaborative reduction initiatives—particularly critical given Scope 3’s dominance of corporate footprints; Integrated ESG reporting platforms consolidating sustainability data with financial and operational information through ERP-centric solutions that improve accuracy, streamline compliance, and reduce reporting burden across multiple frameworks.

Technology deployment should prioritize data quality and interoperability. Eighty-two percent of business leaders report lacking a “single source of truth” for decarbonization data, undermining decision-making and stakeholder confidence. Addressing this requires: Centralized data repositories aggregating information from operational systems, supplier reports, and third-party sources; standardized data taxonomies and emission factors aligned with recognized protocols like the GHG Protocol; automated data validation routines identifying outliers and inconsistencies—critical given prevalence of calculation errors in Scope 3 accounting; and blockchain or similar technologies ensuring data integrity and creating tamper-resistant audit trails supporting external verification.

Bold net-zero commitments must be supported by detailed decarbonization roadmaps functioning as blueprints for action. Effective roadmaps: Identify and prioritize 21+ decarbonization levers spanning energy efficiency (used by 87% of companies), waste reduction (87%), renewables adoption (81%), building-related measures (80%), supplier engagement (79%), and emerging technologies like carbon capture and green hydrogen; sequence implementation considering technical feasibility, cost-effectiveness, interdependencies, and market readiness—recognizing technologies and costs evolve rapidly; quantify emissions impact and financial implications for each lever, developing business cases demonstrating ROI through energy savings, risk mitigation, revenue enhancement, and improved capital access; and establish interim milestones enabling course correction—particularly important given only 14% of companies surveyed combine solutions into comprehensive decarbonization plans achieving stated goals.

Roadmaps must function as living documents adapting to changing circumstances. The rapidly evolving technological landscape—with battery costs declining, renewable energy achieving grid parity, and green hydrogen approaching commercial viability—creates opportunities for acceleration beyond original plans. Conversely, supply chain disruptions, policy changes, and physical climate impacts may necessitate strategy adjustments. Organizations should review and update roadmaps at least annually, incorporating lessons learned, emerging technologies, policy developments, and stakeholder feedback to maintain plans’ relevance and ambition.

No organization can achieve net-zero in isolation. Strategic partnerships amplify impact and share risk across multiple dimensions: Supplier collaboration programs providing technical assistance, financing, and incentives to help key suppliers decarbonize—particularly important given supply chain emissions’ dominance and suppliers’ frequent resource constraints; Industry consortia and pre-competitive collaboration developing sector-specific decarbonization pathways, sharing best practices, and advocating for supportive policies—examples include SBTi sector guidance, industry-specific carbon accounting methodologies, and collaborative research on hard-to-abate emissions; Investor engagement through initiatives like Climate Action 100+ providing access to capital, technical expertise, and accountability mechanisms while amplifying corporate climate ambition through collective pressure; Technology partnerships with solution providers accelerating innovation in carbon accounting software, renewable energy, energy storage, carbon capture, and other enabling technologies; and Research collaborations with universities and national laboratories advancing fundamental science in areas like green chemistry, materials science, and industrial decarbonization where breakthrough innovations are required.

Partnerships prove particularly valuable for addressing Scope 3 complexity. Organizations like the MIT Sustainable Supply Chain Lab are developing standardized methodologies for life-cycle emissions tracking, enhancing accuracy and comparability across sectors. The Partnership for Carbon Accounting Financials (PCAF) provides financial institutions with methodologies for measuring financed emissions, enabling banks and investors to assess and manage climate risks in portfolios. By engaging with these collaborative initiatives, companies access cutting-edge methodologies, benchmarking data, and peer learning opportunities that would be prohibitively expensive to develop independently.

The sustainability transformation landscape will continue evolving rapidly, driven by accelerating climate impacts, technological breakthroughs, regulatory developments, and shifting stakeholder expectations. Several trends merit executive attention as organizations position for long-term success.

Regulatory harmonization proceeds unevenly but inexorably. While the U.S. federal government withdrew climate disclosure requirements in 2025, state-level mandates proliferate, the European Union continues expanding CSRD coverage, and dozens of countries adopt ISSB standards. This fragmentation creates complexity for multinational corporations but also opportunities for differentiation—organizations developing robust, multi-framework reporting capabilities gain competitive advantages in stakeholder trust and regulatory compliance. Anticipated developments include: Scope 3 disclosure requirements expanding as methodologies mature and data quality improves; carbon border adjustment mechanisms (CBAM) proliferating beyond the EU, directly linking emissions to trade competitiveness; enhanced assurance requirements transitioning from limited to reasonable assurance as carbon accounting matures to match financial reporting standards; and nature-related disclosures gaining prominence as frameworks like TNFD gain adoption, expanding corporate accountability beyond carbon to biodiversity and ecosystem impacts.

Technology convergence will transform carbon management from periodic reporting to predictive, prescriptive intelligence. Artificial intelligence, IoT sensors, satellite monitoring, and blockchain verification are integrating into comprehensive platforms providing: Autonomous emissions tracking with minimal manual intervention, dramatically reducing compliance burden; predictive analytics forecasting emissions trajectories under different operational scenarios, enabling proactive management; prescriptive recommendations identifying optimal decarbonization interventions considering cost, impact, and feasibility; and real-time verification through satellite and sensor networks making greenwashing increasingly difficult as third-party monitoring validates corporate claims.

Financial innovation will accelerate as sustainability and financial performance become inseparable. Mechanisms gaining traction include: Sustainability-linked financing where loan terms or bond yields adjust based on emissions performance, aligning capital providers’ and companies’ interests in decarbonization; carbon markets evolving from compliance mechanisms to sophisticated trading platforms with increased liquidity, transparency, and integrity—though voluntary offset markets face quality concerns requiring rigorous standards; green taxonomies defining which economic activities qualify as sustainable, channeling capital toward genuinely beneficial investments while preventing greenwashing; and natural capital accounting incorporating ecosystem services and biodiversity into corporate and national accounts, fundamentally expanding the definition of value creation.

The organizations that thrive in this environment will be those treating sustainability transformation not as a risk to be managed but as a source of competitive advantage to be leveraged.

By investing in robust carbon accounting infrastructure, developing comprehensive decarbonization roadmaps, engaging suppliers and partners, and embedding sustainability into core strategy and operations, forward-thinking companies position themselves to capture the estimated $26.4 trillion in revenue under net-zero commitments while contributing meaningfully to planetary stability.

The question facing executive leadership is not whether to transform, but how quickly and comprehensively to do so—with the window for advantage shrinking as sustainability transformation moves from differentiator to table stakes.

Scope 3 emissions complexity and data quality issues represent the most significant barriers, affecting over 80% of companies pursuing net-zero goals

Doowe has two innovative products across our UK and European operations — Doowe Carbon Accounting *and *Doowe Carbon API. The Carbon Accounting platform helps businesses measure, manage, and report their carbon emissions accurately, while the Carbon API allows seamless integration of carbon data and ESG metrics into digital systems for real-time sustainability tracking.

We’re open to collaborations with organizations or individuals interested in carbon management, sustainability, or ESG consultancy. For enquiries or partnerships, more details can be found at www.doowe.uk

Ready to confidently step into the future of sustainable business? doowe is your reliable partner in this journey, providing expert carbon footprint services to ensure your commitment to the environment is clear, concrete, and verifiable.

Source: www.linkedin.com/pulse