In Africa’s emerging low-carbon economy, carbon is no longer just a pollutant; it’s a price, a policy, and a pathway to competitiveness. Every tonne of CO₂ now carries both a financial and a strategic story: one that links climate risk, corporate performance, and economic resilience. As global markets and regulators increasingly integrate environmental metrics into financial systems, companies that can measure, price, and manage carbon will hold the advantage. Reducing emissions has become synonymous with reducing costs and with unlocking long-term investor confidence.

“Carbon,” in climate policy, represents the family of greenhouse gases expressed as carbon-dioxide equivalents (CO₂e). These include carbon dioxide (CO₂), methane (CH₄), nitrous oxide (N₂O), and fluorinated gases such as hydrofluorocarbons (HFCs) (IPCC, 2021). Carbon accounting refers to the systematic quantification and reporting of these gases across operational and value-chain activities (GHG Protocol, 2015). This process is essential not only for compliance but for strategic management providing data that can shape capital allocation, product design, and brand reputation. As tariffs and carbon taxes rise, the commercial logic of decarbonisation becomes self-reinforcing: lower carbon equals lower cost.

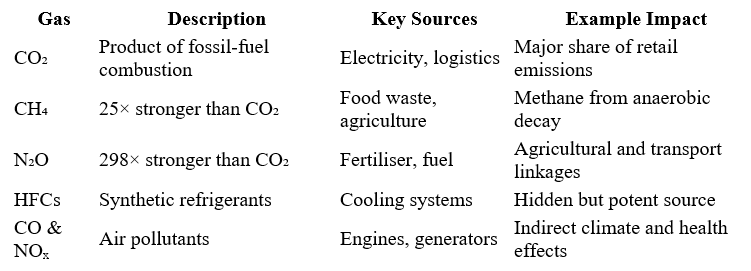

Everyday commerce hides an invisible footprint. From electricity to logistics, each step emits a measurable form of carbon.

For African retailers, the lesson is clear: understanding and measuring these sources is the first step toward sustainable operations and climate-aligned competitiveness.

Across Southern Africa, climate policy is being woven into the fabric of economic transformation. The Southern African Development Community (SADC) has embedded climate mitigation and adaptation in its development strategy, aligning national commitments with the Paris Agreement (UNFCCC, 2015). South Africa has led the way with the Carbon Tax Act (No. 15 of 2019), Africa’s first national carbon tax. It began at R120 per tonne of CO₂e and rose to R159 by 2023, with scheduled annual escalations (National Treasury, 2023). The phased approach allows flexibility through tax-free allowances and verified offsets of up to 10 % of a company’s liability (World Bank, 2023). Meanwhile, initiatives such as the SADC Green Fund and Green Climate Fund Readiness Programme, managed through the Development Bank of Southern Africa (DBSA, 2022), are mobilising finance for low-carbon development. These align with the African Union’s Green Recovery Action Plan (2021–2027), which prioritises renewable-energy investment, reforestation, and climate-resilient infrastructure (African Union, 2021).

South Africa’s carbon-pricing model is now a reference point across SADC. It demonstrates how fiscal tools can drive emissions reduction while protecting economic growth (Koch & Newcombe, 2021). Neighbouring countries trading with South Africa inevitably face indirect carbon exposure through supply chains and exported goods. As the EU’s Carbon Border Adjustment Mechanism (CBAM) takes effect in 2026, alignment with global carbon-accounting standards will become both a regulatory necessity and a market advantage (European Commission, 2023; UNCTAD, 2023).

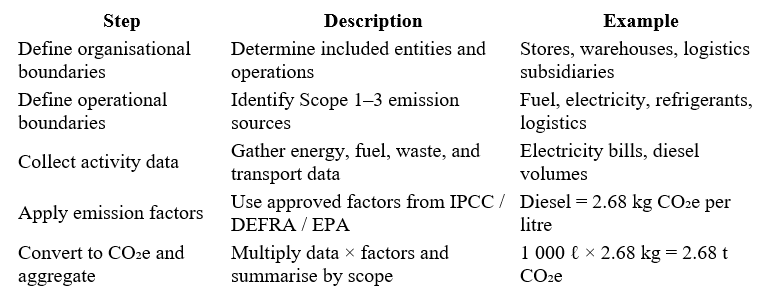

A credible carbon strategy begins with measurement. The GHG Protocol, developed by the World Resources Institute (WRI) and World Business Council for Sustainable Development (WBCSD) remains the global benchmark (GHG Protocol, 2015).

It classifies emissions into:

Key principles include relevance, completeness, consistency, transparency, and accuracy.

Methodology in practice:

This framework aligns with ISO 14064-1 (2018) and the IPCC 2019 Guidelines, ensuring accuracy, comparability, and regulatory compliance (ISO, 2018; IPCC, 2019).

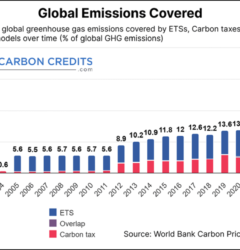

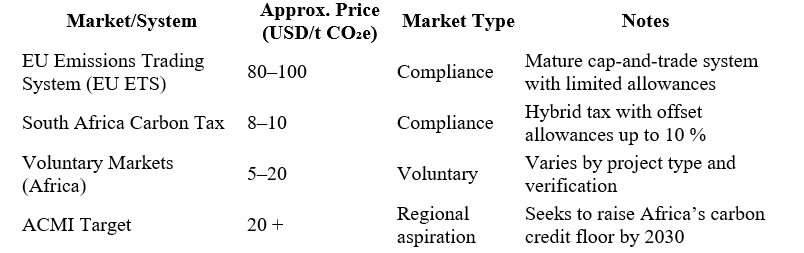

Once emissions are quantified, they can be traded. Carbon markets transform the act of pollution reduction into an economic opportunity. Under the Paris Agreement (UNFCCC, 2015), these markets fall into two main categories:

Indicative carbon prices (2024–2025):

A corporate carbon strategy translates climate data into decision-making. It combines two levers:

Theoretical lenses such as stakeholder theory (Freeman, 1984), institutional theory (DiMaggio & Powell, 1983), and signalling theory (Spence, 1973) explain why credible climate strategies drive legitimacy and investor trust. Transparent carbon reporting signals foresight and lowers perceived risk (Busch et al., 2018).

An Internal Carbon Price (ICP) assigns a monetary value to each tonne of emissions, turning environmental cost into a measurable financial factor (CDP, 2022).

Objectives of ICP:

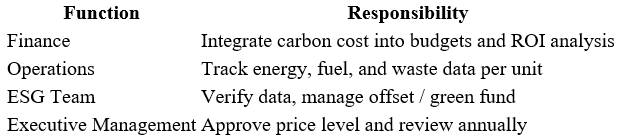

Typical responsibilities:

Linking internal carbon fees to renewable-energy or waste-reduction projects builds both fiscal discipline and long-term value (UNEP FI, 2021; Deloitte, 2022).

A carbon strategy succeeds only when embedded in broader ESG governance. Boards that treat emissions data as strategic information not peripheral disclosure are future-proofing their organisations.

Integration reflects:

Under IFRS S2, companies must disclose transition plans and interim targets, turning climate ambition into measurable governance.

A corporate carbon risk strategy sits at the intersection of environmental accountability, economic rationality, and governance innovation. Its logic is simple: Measure → Manage → Reduce → Offset → Report.

For African firms, this is both a compliance imperative and a strategic opportunity. By quantifying emissions, assigning financial value to carbon, and embedding it within ESG governance, companies can transform climate risk into competitive advantage. In a world where capital increasingly flows toward transparency and sustainability, carbon literacy is becoming the new marker of market leadership.

Doowe has two innovative products across our UK and European operations — Doowe Carbon Accounting *and *Doowe Carbon API. The Carbon Accounting platform helps businesses measure, manage, and report their carbon emissions accurately, while the Carbon API allows seamless integration of carbon data and ESG metrics into digital systems for real-time sustainability tracking.

We’re open to collaborations with organizations or individuals interested in carbon management, sustainability, or ESG consultancy. For enquiries or partnerships, more details can be found at www.doowe.uk

Ready to confidently step into the future of sustainable business? doowe is your reliable partner in this journey, providing expert carbon footprint services to ensure your commitment to the environment is clear, concrete, and verifiable.

Source: www.linkedin.com/pulse

Written by Anushka Bogdanov, Founder of Risk Insights

African Union (2021). Green Recovery Action Plan (2021–2027). Addis Ababa: African Union Commission.

Busch, T., & Lewandowski, S. (2018). Corporate Carbon and Financial Performance: A Meta-Analysis. Journal of Industrial Ecology, 22(4), 745–759.

Carbon Disclosure Project (CDP) (2022). Internal Carbon Pricing Report 2022. London: CDP.

Deloitte (2022). Carbon Accounting and Internal Carbon Pricing: Pathways for Decarbonisation. London: Deloitte Insights.

Department for Environment, Food & Rural Affairs (DEFRA) (2023). UK Government GHG Conversion Factors for Company Reporting. London: DEFRA.

Development Bank of Southern Africa (DBSA) (2022). SADC Green Climate Fund Readiness Programme and Green Fund Overview. Johannesburg: DBSA.

DiMaggio, P.J. & Powell, W.W. (1983). The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. American Sociological Review, 48(2), 147–160.

European Commission (2023). EU Carbon Border Adjustment Mechanism (CBAM): Regulation (EU) 2023/956. Brussels: European Union.

Freeman, R.E. (1984). Strategic Management: A Stakeholder Approach. Boston: Pitman.

Gold Standard Foundation (2023). Certification and Verification Methodologies for Voluntary Carbon Markets. Geneva: Gold Standard.

Greenhouse Gas Protocol (GHG Protocol) (2015). Corporate Accounting and Reporting Standard (Revised Edition). Washington, DC: World Resources Institute and World Business Council for Sustainable Development.

Intergovernmental Panel on Climate Change (IPCC) (2019). 2019 Refinement to the 2006 IPCC Guidelines for National Greenhouse Gas Inventories. Geneva: IPCC.

Intergovernmental Panel on Climate Change (IPCC) (2021). Sixth Assessment Report: Summary for Policymakers (AR6 – Working Group I). Geneva: IPCC.

International Carbon Action Partnership (ICAP) (2024). Status Report: Emissions Trading Worldwide 2024. Berlin: ICAP.

International Organization for Standardization (ISO) (2018). ISO 14064-1:2018 — Greenhouse Gases – Specification with Guidance at the Organization Level for Quantification and Reporting of Greenhouse Gas Emissions and Removals. Geneva: ISO.

Koch, H. & Newcombe, K. (2021). Carbon Taxation in South Africa: Lessons for Emerging Markets. South African Journal of Economic Policy, 38(2), 203–218.

National Treasury (2023). Carbon Tax Rate and Fuel Levy Adjustments 2023/24. Pretoria: Republic of South Africa.

Republic of South Africa (2019). Carbon Tax Act, No. 15 of 2019. Government Gazette No. 42483, 23 May 2019. Pretoria: Government Printer.

South African Reserve Bank (2024). Carbon Taxation in South Africa and the Risks of Carbon Border Adjustment Mechanisms. Occasional Bulletin of Economic Notes, April 2024.

Spence, M. (1973). Job Market Signaling. Quarterly Journal of Economics, 87(3), 355–374.

Suchman, M.C. (1995). Managing Legitimacy: Strategic and Institutional Approaches. Academy of Management Review, 20(3), 571–610.

Tietenberg, T. & Lewis, L. (2018). Environmental and Natural Resource Economics (11th ed.). New York: Routledge.

United Nations Conference on Trade and Development (UNCTAD) (2023). World Investment Report 2023: Investing in Sustainable Energy for All. Geneva: UNCTAD.

United Nations Development Programme (UNDP) (2022). Carbon Pricing and Climate Finance in Sub-Saharan Africa: Regional Readiness Assessment. New York: UNDP.

United Nations Economic Commission for Africa (UNECA) (2022). African Carbon Markets Initiative (ACMI): Building a Scalable Voluntary Carbon Market for Africa. Addis Ababa: UNECA.

United Nations Environment Programme Finance Initiative (UNEP FI) (2021). Gearing up for Water Risk: Addressing Water as a Financial Risk and Opportunity. Geneva: UNEP FI.

United Nations Framework Convention on Climate Change (UNFCCC) (2015). The Paris Agreement. Bonn: UNFCCC.

World Bank (2023). State and Trends of Carbon Pricing 2023. Washington, DC: World Bank Group.